Bronze vs. Silver ACA Plans: Which Metal Tier Is Right for You?

A complete 2026 guide to comparing premiums, deductibles, and cost-sharing reductions across ACA metal tiers.

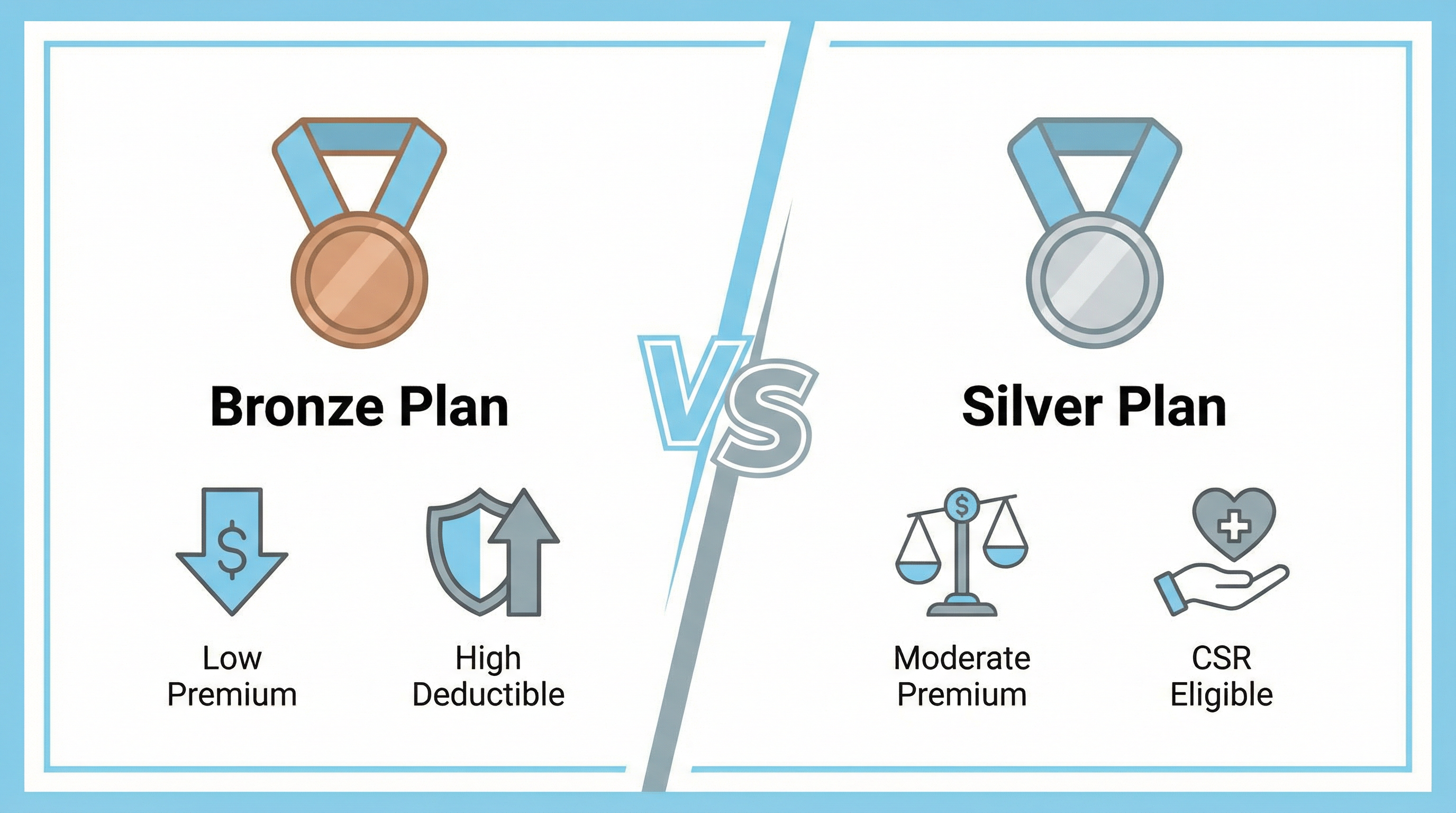

Understanding the ACA Metal Tier System

When you shop for health insurance on the Affordable Care Act (ACA) Marketplace, every plan is organized into one of four metal tiers: Bronze, Silver, Gold, or Platinum. These tiers do not reflect the quality of care you receive — every ACA-compliant plan covers the same 10 essential health benefits. Instead, the metal tier describes how costs are split between you and your insurance company over the course of a plan year.

The two most popular tiers are Bronze and Silver, and choosing between them is one of the most consequential decisions you will make during Open Enrollment. The right choice depends on your health needs, your income, and whether you qualify for a powerful savings program called Cost-Sharing Reductions (CSRs). This guide gives you the complete picture.

The Core Difference: Actuarial Value

The fundamental metric that separates metal tiers is actuarial value (AV) — the percentage of total average medical costs a plan is designed to pay for a standard population. A Bronze plan has an AV of 60%, meaning the plan pays 60 cents of every dollar in covered medical costs on average, and you pay the remaining 40 cents through deductibles, copayments, and coinsurance. A Silver plan has an AV of 70%, shifting more of the financial burden to the insurer.

Key Insight: Actuarial value is an average across all enrollees. Your personal cost-sharing will vary based on how much healthcare you actually use during the year. A healthy person who rarely sees a doctor may pay far less than the 40% implied by a Bronze plan's AV.

2026 Bronze vs. Silver Plan Comparison

| Feature | Bronze Plan | Silver Plan |

|---|---|---|

| Actuarial Value | 60% | 70% |

| Monthly Premium | Lowest | Moderate |

| Typical Deductible | $5,000 – $7,500 | $2,000 – $4,500 |

| Copay (Primary Care) | $50 – $75 after deductible | $30 – $50 (often before deductible) |

| Out-of-Pocket Maximum (2026) | Up to $9,450 (individual) | Up to $9,450 (individual) |

| CSR Eligible? | No | Yes (if income qualifies) |

| Best For | Healthy, low-utilization individuals | Most people, especially CSR-eligible enrollees |

When a Bronze Plan Makes Sense

A Bronze plan is the right choice when your primary goal is the lowest possible monthly premium and you are confident you will not need significant medical care during the year. Bronze plans are designed as a financial safety net — they protect you from catastrophic medical bills while keeping your monthly costs minimal.

Consider a Bronze plan if you are a generally healthy individual in your 20s or 30s with no chronic conditions, no regular prescriptions, and no planned medical procedures. If you go through the entire year with only a few preventive care visits (which are covered at no cost on all ACA plans), a Bronze plan can save you hundreds of dollars in premiums compared to a Silver plan.

However, it is critical to understand the risk: if you do get sick or injured, you will face a very high deductible before your insurance begins to pay. A Bronze plan with a $6,000 deductible means you are responsible for the first $6,000 of medical bills in a year. You must be financially prepared to cover that amount if an unexpected health event occurs.

When a Silver Plan Is the Smarter Choice

For the majority of ACA enrollees, a Silver plan offers better overall value — and for those who qualify for Cost-Sharing Reductions, it is almost always the superior choice by a significant margin.

Silver plans have a higher monthly premium than Bronze, but they come with a lower deductible and lower copayments. If you visit a doctor more than a few times per year, take prescription medications, or have any ongoing health needs, the lower out-of-pocket costs of a Silver plan will likely save you more money than you spend on the higher premium.

The Silver Plan's Unique Advantage: Cost-Sharing Reductions (CSRs)

This is the single most important factor in the Bronze vs. Silver decision for millions of Americans. Cost-Sharing Reductions are only available on Silver plans. If your household income falls between 100% and 250% of the Federal Poverty Level (FPL), you are eligible for CSRs — and they can be transformative.

CSRs automatically reduce your deductible, copayments, and coinsurance when you enroll in a Silver plan. The result is that a CSR-enhanced Silver plan can function like a Gold or even Platinum plan, but you only pay the premium for a Silver plan (which is also reduced by your premium tax credit).

2026 CSR Income Eligibility Thresholds

| Household Size | 100%–150% FPL (Strongest CSR) | 151%–200% FPL (Moderate CSR) | 201%–250% FPL (Basic CSR) |

|---|---|---|---|

| 1 Person | $15,060 – $22,590 | $22,591 – $30,120 | $30,121 – $37,650 |

| 2 People | $20,440 – $30,660 | $30,661 – $40,880 | $40,881 – $51,100 |

| 3 People | $25,820 – $38,730 | $38,731 – $51,640 | $51,641 – $64,550 |

| 4 People | $31,200 – $46,800 | $46,801 – $62,400 | $62,401 – $78,000 |

Source: 2026 HHS Federal Poverty Guidelines. Figures are approximate.

Real-World CSR Example

Consider a single adult earning $22,000 per year (approximately 130% of FPL). Without CSRs, a standard Silver plan might have a $3,500 deductible and a $50 primary care copay. With CSRs applied, that same Silver plan could have a $300 deductible and a $5 primary care copay. The plan pays a dramatically higher share of costs — and the monthly premium is also reduced by a premium tax credit. This is why financial advisors and insurance experts consistently recommend Silver plans for CSR-eligible individuals.

Bottom Line: If your income qualifies you for Cost-Sharing Reductions, choosing a Bronze plan means you are leaving significant government assistance on the table. The CSR benefit is only accessible through a Silver plan, and it can be worth thousands of dollars per year in reduced medical costs.

The Total Cost Calculation: Don't Just Look at the Premium

A common mistake during Open Enrollment is choosing a plan based solely on the monthly premium. The true cost of a health plan is the sum of your annual premiums plus your actual out-of-pocket costs for the care you use. To make an informed decision, you need to estimate your total annual cost under each plan scenario.

For example, if a Bronze plan saves you $80 per month in premiums ($960 per year) compared to a Silver plan, but you end up needing $2,000 worth of medical care that you pay out-of-pocket due to the higher Bronze deductible, you would have been better off with the Silver plan. Running this calculation based on your expected healthcare usage is the most reliable way to choose the right tier.

How to Make Your Final Decision

Use the following framework to guide your choice between Bronze and Silver for 2026:

- Check your CSR eligibility first. If your income is between 100% and 250% of the FPL, a Silver plan with CSRs is almost certainly your best option. Do not choose Bronze without first understanding what CSRs would do to your Silver plan's costs.

- Estimate your healthcare usage. Think honestly about how many doctor visits, specialist appointments, and prescriptions you expect in 2026. The more care you anticipate needing, the more valuable a lower deductible becomes.

- Calculate your total annual cost. Add up 12 months of premiums plus your estimated out-of-pocket costs for each plan you are considering. Compare the totals, not just the monthly premiums.

- Consider your financial cushion. If you cannot comfortably afford to pay a $5,000–$7,000 deductible in the event of a medical emergency, a Bronze plan carries real financial risk for you.

Our FFM-certified agents can walk you through this calculation for free and help you identify the plan that offers the best combination of coverage and value for your specific situation. Call us at 888-982-0356 or fill out the form above to get started.

Ready to Find the Right Health Plan?

Our FFM-certified agents are standing by to help you compare plans, calculate your subsidies, and enroll in minutes. There is no cost to use our service.

Get Free Quote Now Call 888-982-0356