HMO vs. PPO ACA Plans in 2026: A Complete Side-by-Side Comparison

Network flexibility, referral requirements, costs, and which plan type fits your lifestyle.

The Two Most Common ACA Plan Types

When you shop for health insurance on the ACA Marketplace, you will encounter several types of plan structures. The two most common are Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Both are ACA-compliant and cover the same essential health benefits. The difference lies in how they manage your access to care — specifically, which doctors you can see, whether you need referrals, and what happens if you go outside the plan's network.

Understanding the difference between these plan types is essential for choosing a plan that fits your lifestyle, your existing doctor relationships, and your budget.

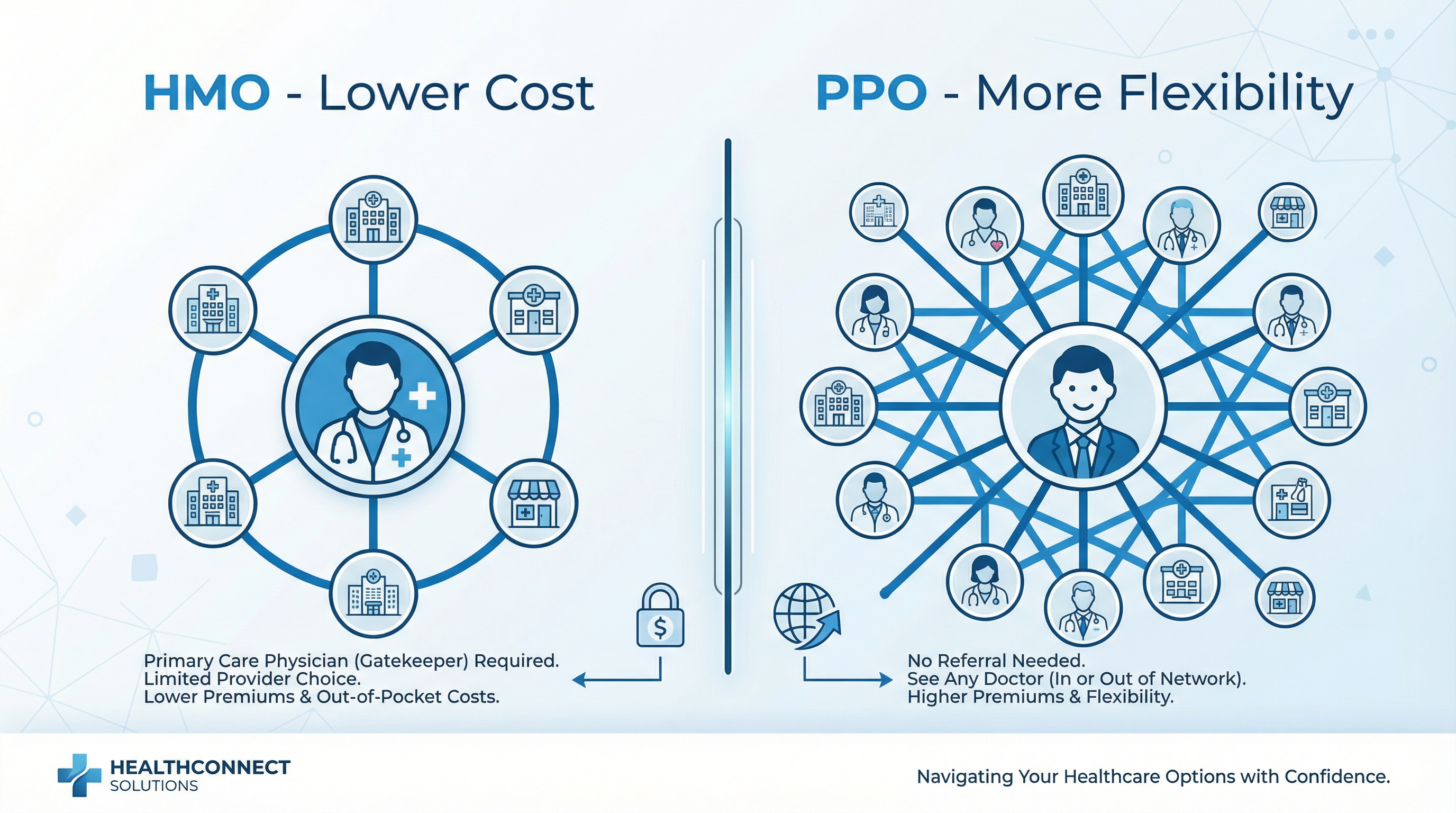

HMO vs. PPO: The Core Differences at a Glance

| Feature | HMO | PPO |

|---|---|---|

| Monthly Premium | Lower | Higher |

| Deductible | Lower to Moderate | Moderate to Higher |

| Primary Care Physician (PCP) Required? | Yes — must choose a PCP | No — optional |

| Referrals to See Specialists? | Yes — required from PCP | No — see any in-network specialist directly |

| Out-of-Network Coverage? | No (except emergencies) | Yes — at higher cost |

| Network Size | Smaller, more defined | Larger, more flexible |

| Administrative Simplicity | Simpler (one point of contact) | More complex (track in vs. out-of-network) |

| Best For | Budget-conscious; those with a trusted PCP | Those who want flexibility and specialist access |

How HMO Plans Work

In an HMO, you select a primary care physician (PCP) from the plan's network. Your PCP becomes your central point of contact for all of your health care. When you need to see a specialist — a cardiologist, dermatologist, orthopedist, etc. — your PCP must provide a referral. Without a referral, the specialist visit may not be covered.

HMOs do not cover care from out-of-network providers, except in genuine medical emergencies. This means that if you see a doctor who is not in your HMO's network, you will likely be responsible for the full cost of that visit. This network restriction is the primary trade-off for the HMO's lower premiums and simpler cost structure.

HMOs work best for people who have an established relationship with a primary care doctor who is in the plan's network, who do not need to see specialists frequently, and who are comfortable with the referral process. They are also a good choice for families with children, where the pediatrician serves as the central coordinator of care.

How PPO Plans Work

In a PPO, you have the freedom to see any doctor or specialist — in-network or out-of-network — without a referral. You do not need to choose a primary care physician, though you may choose to have one. This flexibility is the defining feature of a PPO and the primary reason people choose them despite their higher premiums.

When you use in-network providers, you pay the lower in-network cost-sharing rates. When you use out-of-network providers, you pay higher rates — but the plan still covers a portion of the cost. This is a critical difference from an HMO, where out-of-network care is simply not covered (except in emergencies).

PPOs are the right choice for people who see multiple specialists, have established relationships with doctors who may not all be in the same network, travel frequently and need coverage flexibility, or simply value the freedom to seek care without administrative barriers.

EPO Plans: A Middle Ground

A third plan type worth knowing is the Exclusive Provider Organization (EPO). An EPO combines features of both HMOs and PPOs: like a PPO, it does not require referrals to see specialists. But like an HMO, it does not cover out-of-network care except in emergencies. EPOs typically have premiums between HMO and PPO levels. They are a good option for people who want specialist flexibility without the higher cost of a full PPO.

The Referral Process: What It Actually Means in Practice

Many people are deterred by the HMO referral requirement, but in practice it is less burdensome than it sounds for most patients. Your PCP can typically send a referral electronically, and in many cases you can request one over the phone or through a patient portal without an office visit. The referral process does add a step, but for routine specialist care, it is rarely a significant obstacle.

Where the referral requirement becomes genuinely problematic is in urgent situations — when you need to see a specialist quickly and cannot wait for a referral to be processed. If you have a condition that requires frequent, time-sensitive specialist access, a PPO or EPO may serve you better.

Cost Comparison: Which Is Cheaper Overall?

The answer depends entirely on how much care you use. If you rarely need medical care beyond preventive services and your PCP is in-network, an HMO will almost always be cheaper — the lower premium savings compound significantly over a full year. If you use specialists frequently or need out-of-network flexibility, a PPO's higher premium may be offset by the avoidance of out-of-network bills and the elimination of referral delays.

The best approach is to calculate your estimated total annual cost (premium + out-of-pocket costs) for each plan type based on your expected healthcare usage, as described in our Health Plan Comparison Guide. Our agents can help you run this calculation for the specific plans available in your area. Call 888-982-0356 for free assistance.

Ready to Find the Right Health Plan?

Our FFM-certified agents are standing by to help you compare plans, calculate your subsidies, and enroll in minutes. There is no cost to use our service.

Get Free Quote Now Call 888-982-0356