Short-Term Health Insurance vs. ACA Plans in 2026: What You Need to Know

The critical differences in coverage, pre-existing condition rules, and when a short-term plan is — and isn't — appropriate.

What Is Short-Term Health Insurance?

Short-term health insurance is a type of limited-duration health coverage designed to bridge temporary gaps in insurance. These plans are not ACA-compliant, which means they are exempt from many of the consumer protections and coverage requirements that apply to Marketplace plans. They are typically cheaper than ACA plans, but they come with significant limitations that can leave you exposed to substantial financial risk.

Under federal rules, short-term plans can cover an initial period of up to 3 months, with the option to renew for up to a total of 4 months. However, some states have different rules — some allow longer durations, while others have banned or heavily restricted short-term plans. The regulatory landscape for short-term plans has shifted in recent years, so it is important to understand the current rules in your state.

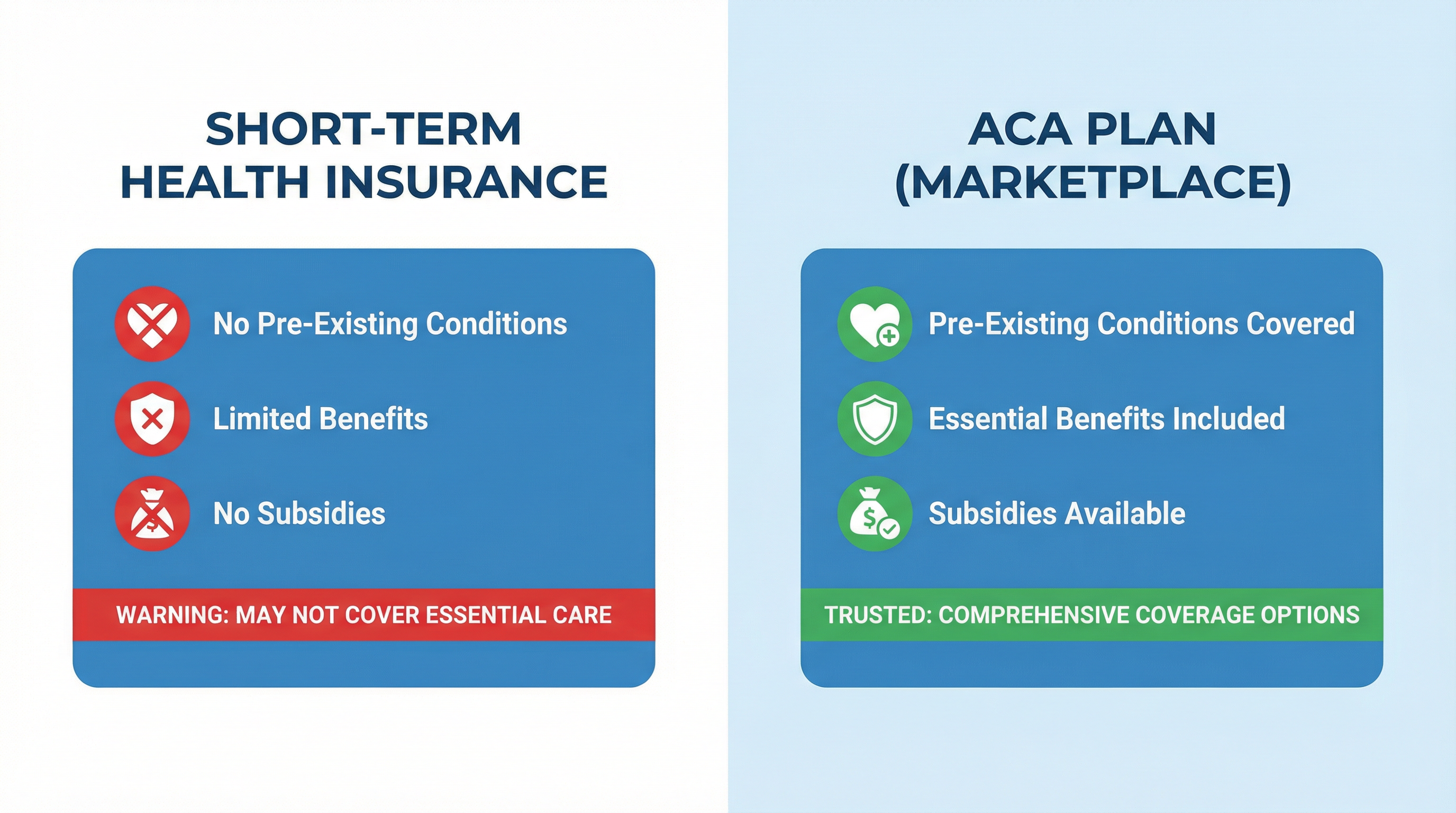

The Critical Differences: ACA vs. Short-Term Plans

| Feature | ACA Marketplace Plan | Short-Term Health Plan |

|---|---|---|

| Pre-Existing Conditions | Must be covered; cannot be excluded | Can be excluded entirely |

| Essential Health Benefits | All 10 EHBs required | Not required; often excluded |

| Mental Health Coverage | Required | Often excluded or very limited |

| Prescription Drug Coverage | Required | Often excluded or very limited |

| Maternity Coverage | Required | Almost always excluded |

| Annual/Lifetime Benefit Limits | Prohibited | Common; can leave you with large bills |

| Premium Tax Credits | Available (income-based) | Not eligible |

| Monthly Premium | Varies; often low with subsidies | Often lower (but less coverage) |

| Duration | Annual; renewable | Up to 4 months (federal limit) |

| State Mandate Compliance | Qualifies in all states | Does NOT qualify in mandate states |

The Pre-Existing Condition Problem

The most significant risk of short-term health insurance is its treatment of pre-existing conditions. Unlike ACA plans, which are required to cover pre-existing conditions without exclusion or additional cost, short-term plans can — and routinely do — deny claims related to any condition you had before the policy began.

The definition of a "pre-existing condition" used by short-term insurers is often very broad. A condition does not have to be formally diagnosed to be considered pre-existing — if you had symptoms, sought treatment, or even just discussed a health concern with a doctor in the months or years before your short-term policy began, the insurer may deny claims related to that condition. This can result in enormous unexpected medical bills for people who thought they were covered.

Real-World Risk: A person who purchases a short-term plan and is later diagnosed with cancer, diabetes, or heart disease may find that their insurer denies coverage for treatment, citing a pre-existing condition exclusion. The result can be hundreds of thousands of dollars in uninsured medical bills. This is not a theoretical risk — it happens regularly to short-term plan enrollees.

When Short-Term Plans Are Appropriate

Despite their limitations, there are narrow circumstances where a short-term plan may be a reasonable choice:

- You are in a very brief coverage gap (a few weeks) between two comprehensive plans and you are in excellent health with no ongoing medical needs.

- You missed Open Enrollment, do not have a qualifying life event for a Special Enrollment Period, and cannot access Medicaid — and you need some form of protection against catastrophic medical costs while you wait for the next Open Enrollment Period.

- You are a young, healthy adult with no pre-existing conditions, no regular medications, and no planned medical procedures, and you have fully understood and accepted the coverage limitations.

In all of these cases, you should first exhaust all other options — including checking for Medicaid eligibility, verifying whether you have a qualifying life event for a Special Enrollment Period, and exploring whether a spouse's employer plan is available.

The Better Alternative: ACA Special Enrollment

Many people who consider short-term plans do so because they believe they have missed their window to enroll in an ACA plan. But qualifying life events — including losing job-based coverage, moving to a new area, getting married, or having a baby — trigger a 60-day Special Enrollment Period on the Marketplace. If you have experienced any of these events, you may be able to enroll in a comprehensive ACA plan right now, without waiting for Open Enrollment.

Before purchasing a short-term plan, call our agents at 888-982-0356 to determine whether you qualify for a Special Enrollment Period. In many cases, people who think they are stuck without options actually have a path to comprehensive, subsidized ACA coverage.

Ready to Find the Right Health Plan?

Our FFM-certified agents are standing by to help you compare plans, calculate your subsidies, and enroll in minutes. There is no cost to use our service.

Get Free Quote Now Call 888-982-0356