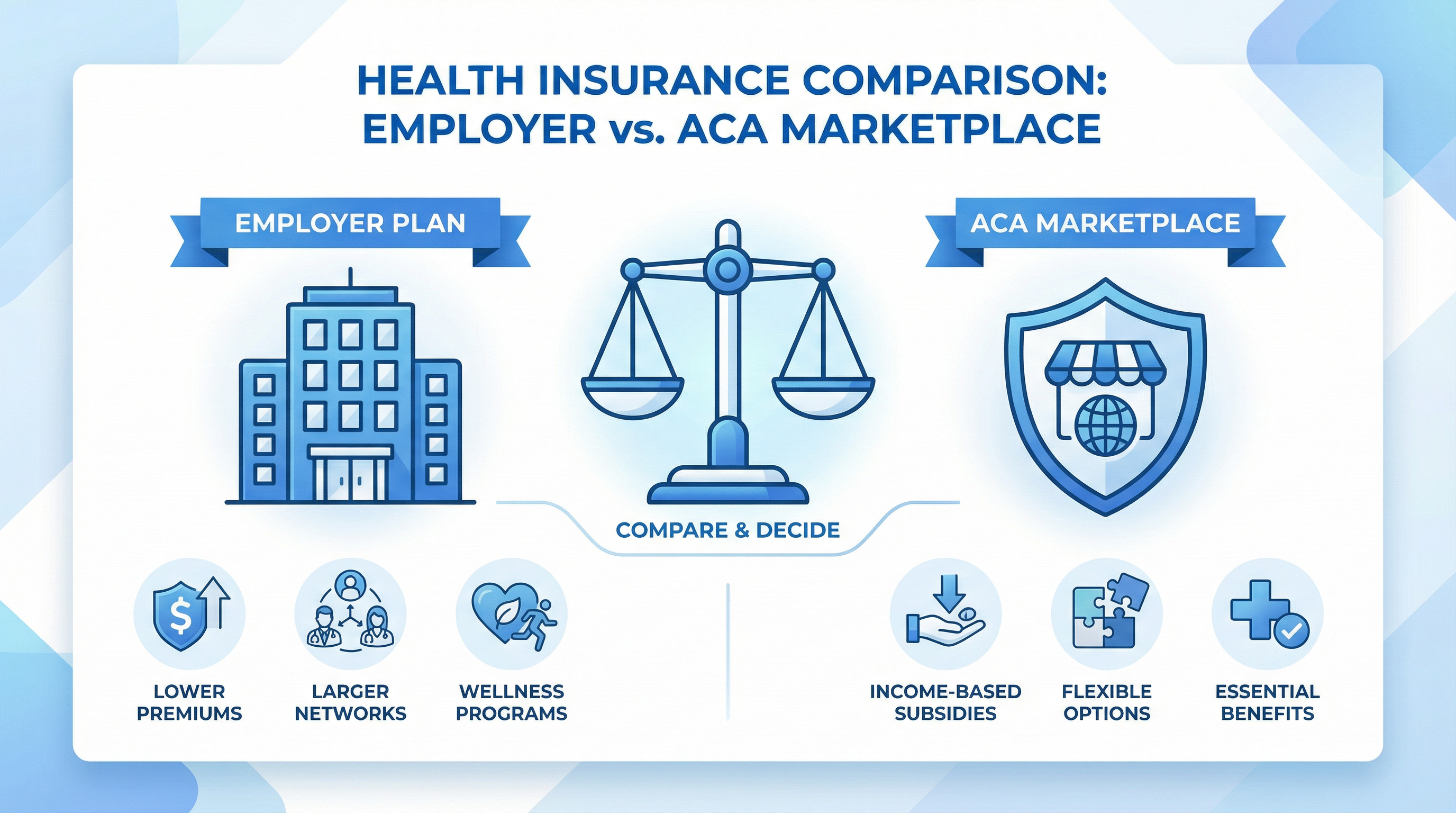

Employer Coverage vs. ACA Marketplace: How to Make the Right Choice in 2026

The affordability test, the family glitch fix, and when a Marketplace plan beats your employer's offer.

The Default Assumption — and Why It's Often Wrong

Most Americans assume that if their employer offers health insurance, they should take it. For many people, this is the right choice. But it is not always the right choice, and millions of workers are overpaying for health coverage because they never stopped to compare their employer's plan against what is available on the ACA Marketplace.

The key factors that determine which option is better for you are: the cost of your employer's plan, the quality of its benefits and network, your household income, and whether you qualify for ACA subsidies. This guide walks you through the comparison framework step by step.

The ACA Affordability Test: The Most Important Calculation

Your eligibility for premium tax credits on the ACA Marketplace is directly tied to whether your employer's plan is considered "affordable" under ACA rules. If your employer offers a plan that passes the affordability test, you are generally not eligible for Marketplace subsidies — even if you think the plan is expensive.

For 2026, an employer-sponsored plan is considered affordable if the employee's share of the premium for the lowest-cost, self-only plan is less than 9.02% of the employee's household income. (This percentage is adjusted annually by the IRS.)

Affordability Example: If your household income is $50,000 per year, your employer's plan is considered affordable if your monthly premium for self-only coverage is less than $375.83/month ($50,000 × 9.02% ÷ 12). If your premium is $400/month, the plan is technically unaffordable, and you may be eligible for Marketplace subsidies.

The "Family Glitch" Fix: A Game-Changer for Families

Prior to 2023, the affordability test was applied only to the cost of the employee's self-only coverage, even when determining subsidy eligibility for the entire family. This meant that even if adding a spouse and children to an employer plan cost $1,500/month, the family was still considered to have access to affordable coverage and was ineligible for Marketplace subsidies — simply because the employee's own coverage was affordable.

This was known as the "family glitch," and it left millions of families without access to affordable coverage. The Biden administration fixed this rule in 2023, and the fix remains in effect for 2026. Now, the affordability of family coverage is tested separately. If the cost of adding family members to the employer plan exceeds 9.02% of household income, those family members may be eligible for subsidized Marketplace coverage — even while the employee remains on the employer plan.

Head-to-Head Comparison: Employer Plan vs. ACA Marketplace

| Factor | Employer-Sponsored Plan | ACA Marketplace Plan |

|---|---|---|

| Premium Cost | Often lower due to employer contribution | Can be $0–$50/month with subsidies |

| Plan Choice | Limited to what employer offers | Multiple carriers and metal tiers |

| Provider Network | Fixed by employer's plan selection | You choose the network that fits your doctors |

| Financial Assistance | Employer contribution only | Premium tax credits + CSRs (income-based) |

| Portability | Lost when you leave the job | Stays with you regardless of employment |

| Family Coverage Cost | Can be very expensive | Subsidies based on total household income |

When the ACA Marketplace Wins

There are four common scenarios where the ACA Marketplace is likely to be the better financial choice:

Scenario 1: Your Employer's Plan Fails the Affordability Test

If your self-only premium exceeds 9.02% of your household income, your employer's plan is unaffordable under ACA rules, and you are eligible for Marketplace subsidies. In this case, you should almost certainly compare Marketplace options before accepting your employer's plan.

Scenario 2: Family Coverage Is Prohibitively Expensive

Thanks to the family glitch fix, if the cost of adding your family to your employer plan exceeds the affordability threshold, your family members can get subsidized Marketplace coverage. This can result in significant savings for families where the employer plan's family premium is very high.

Scenario 3: Your Employer's Network Doesn't Include Your Doctors

If your employer's plan has a narrow network that excludes your primary care physician, specialists, or preferred hospital, a Marketplace plan with a broader network may offer better practical value — even at a higher premium.

Scenario 4: Your Income Qualifies You for Significant Subsidies

If your household income is below 250% of the FPL and your employer's plan is unaffordable, a CSR-enhanced Silver plan on the Marketplace could provide Gold-level benefits at a fraction of the cost of your employer's plan.

How to Make the Comparison

- Get the exact premium cost for your employer's lowest-cost self-only plan and the lowest-cost family plan.

- Apply the 9.02% affordability test to both figures using your household income.

- Visit the Marketplace and complete an application to see what plans and subsidies are available to you.

- Compare the total annual cost (premiums + estimated out-of-pocket costs) for your top employer plan option and your top Marketplace option.

- Consider non-cost factors: network quality, plan flexibility, and portability.

Our agents can run this comparison for you in minutes and give you a clear recommendation based on your specific numbers. Call 888-982-0356 for a free consultation.

Ready to Find the Right Health Plan?

Our FFM-certified agents are standing by to help you compare plans, calculate your subsidies, and enroll in minutes. There is no cost to use our service.

Get Free Quote Now Call 888-982-0356